The recent announced proposal to merge three public sector banks — Bank of Baroda, Vijaya Bank and Dena Bank — is a step further towards the consolidation of banking sector in India. While the announcement was made on September 17 by the Union Finance Minister Arun Jaitly, the regulatory processes are expected to be completed by the end of financial year 2018-19.

The recent announced proposal to merge three public sector banks — Bank of Baroda, Vijaya Bank and Dena Bank — is a step further towards the consolidation of banking sector in India. While the announcement was made on September 17 by the Union Finance Minister Arun Jaitly, the regulatory processes are expected to be completed by the end of financial year 2018-19.

The proposal had been evolved by the Alternative Mechanism, comprising Union Ministers Arun Jaitley, Nirmala Sitharaman and Piyush Goyal — when formalised — it would produce the third largest lender in India. The approval framework for mergers of SBI and five associate banks along with Bhartiya Mahila Bank (that came into effect from April 1,2017) ; takeover of IDBI by Life Insurance Corporation of India and amalgamation of Bank of Baroda, Vijaya Bank and Dena Bank were prepared by the Alternative Mechanism.

All the three attempts have been made to integrate loss making entities with the healthy players to create operational synergies. The public sector banks command a dominant share and presence in the Indian economy and any restructuring in banking entities with majority stake of government has ramifications not only on those who are directly concerned, but also on the entire eco-system.

While the consolidation of banks in India was suggested by Narasimham Committee on banking reforms way back in 1990s, the recommended degree of consolidation remained tardy due to lack of government impetus. It had recommended three-tier banking structure in India through carving out three large banks with global footprint, eight to ten banks having pan-India operations and large number of regional and local banks. The committee also advocated the Non-Performing Assets to be brought down to 3% by the year 2002.

The banking sector in India has been navigating through turbulent time. The negative spillovers from the global markets, less than adequate demand for credit in the domestic market, sluggish exports, stress in steel, power and infrastructure sector and subdued confidence of investors have largely contributed towards rising non-performing assets.

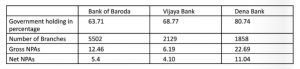

Among the three entities proposed to be merged; Bank of Baroda and Vijaya Bank have healthy balance sheets with gross NPAS of 12.46 per cent and 6.19 per cent and net NPAs of 5.4 per cent and 4.1 per cent respectively. The third institution, Dena Bank reportedly has 22.69 per cent gross and 11 per cent net NPAs, evidently seeking a bailout to save itself from collapse.

A big question about the outcome of the amalgamation of banks has also been raised by those who dissent this move. The gross NPAs of State Bank of India have shot up post merger from 1.12,343 on 31st December 2016 to 1.99,441 on 31st December 2017 to 2,23,427 cr on 31st March 2018 as per an RTI reply by SBI.

The major culprit in the rise of toxic loans was the stalled power and infrastructure projects that culminated into delayed repayments and non-service of debts. High business activity from year 2000 to 2006 resulted in over projection and banks accepting higher leverage in projects and less promoter equity. The sentiments were so high that sometimes banks even outsourced the due diligence and project analysis to the outfits of promoters’ choice. This over confidence pushed the banks into the quagmire of sour assets.

Government has a majority stake in 21 private sector banks and this accounts for two-third of the assets of banking industry. The total NPAs of the banking sector stands at 10 lakh crore as on the end of financial year 2017-18, with public sector banks contributing a colossal 90% of the total NPAs that amounts to 8.9 lakh crore. Out of these 21 banks, 11 are currently under the PCA (Prompt Corrective Action of Reserve Bank of India); thus have restrictions on lending, distribution of dividends and profits (if they have any) and provisioning of sour loans.

The Finance Minister Arun Jaitley, during Annual Performance Review Meeting of Public Sector Banks on September 25 sought the feedback of the bankers on various issues to improve the performance ailing banking sector. The bankers, during the meeting, solicited relaxation in PCA framework to resolve the snags in lending activity. The PCA guidelines, according to bankers, were creating obstacles to achieve the conformity with the Basel III (an internationally agreed set of measures on bank capital adequacy, stress testing and market liquidity risk), that has to be fully implemented by March 2019. It has been reported that PSBs have requested the Finance Minister for relaxation net Non-Performing Asset criteria and Minimum Capital Requirement of banks falling under the ambit of PCA framework.

Giving a banker’s perspective on mergers, Saravjit Singh Samra, Managing Director of Capital Local Area Bank, said that the amalgamation of banks may have some challenges in short-run, but it would give a vigour to the banking industry in the long-run. He added that India is a vast country with diverse needs; the large banks have different focus area to match the growing needs of the economy. The Capital Local Area Bank, the first Small Finance Bank of India launched in April 2016 posted Gross NPA of 1.17 per cent and Net NPA of 0.85 per cent of the total advances as on June 30, 2018.

“Three basic tools, if used prudently, can save a bank from falling into trap of bad loans and these are equally applicable to large and small banks. To assess the intentions of the borrower is the most essential parameter on which lending has to be decided. The repayment capacity should be evaluated; here the need to probe the past track record of the borrower is crucial. Finally, the end use of the loan should be examined thoroughly. The loan should be raised for the productive purpose, to enhance the income level of the borrower,” said Samara.

There is enough evidence that the undue political and bureaucratic interference in decision making at different levels has been responsible to the present state of affairs in banking sector in India. This can be corroborated by the note submitted by the former Governor of Reserve Bank of India, Raghuram Rajan to Chairman of Estimates Committee, Murli Manohar Joshi. He blamed the slow decision making at the Centre during the regimes of UPA and the present NDA Government for magnifying the malady of bad loans. In the note, Rajan has reportedly suggested need of improving governance of PSBs and stricter norms for project evaluation and monitoring the lending process.

Though rules are in place, but unfortunately all the rules and guidelines designed to curb the NPAs are applied in letter and spirit on small ticket borrowers who mortgage their assets of value more than the amount borrowed. The big ticket borrowers come with a recommendation from the power wielders of the system and the funds meant are appropriated by the recalcitrant borrowers. The former RBI Governor had also informed the Parliament that a list of high-profile defaulters was sent to the Prime Minister Office to take action but of no consequence. The RBI’s Financial Stability Report had earlier this year said that larger borrower accounted for 54.8 per cent of the gross advances and 85.6 per cent of gross NPAs.

The schemes announced in favour of small industries and agriculture like MUDRA loans and Kisan Credit Cards need scrutiny as Rajan had cautioned for the next phase of banking crisis from these segments. But it needs a deeper analysis as the per capita loan in this category is minimal as compared to the big defaulters and the credit leakages at different levels undermine the repaying capacity of the small borrowers.

letters@tehelka.com

{kind=link}